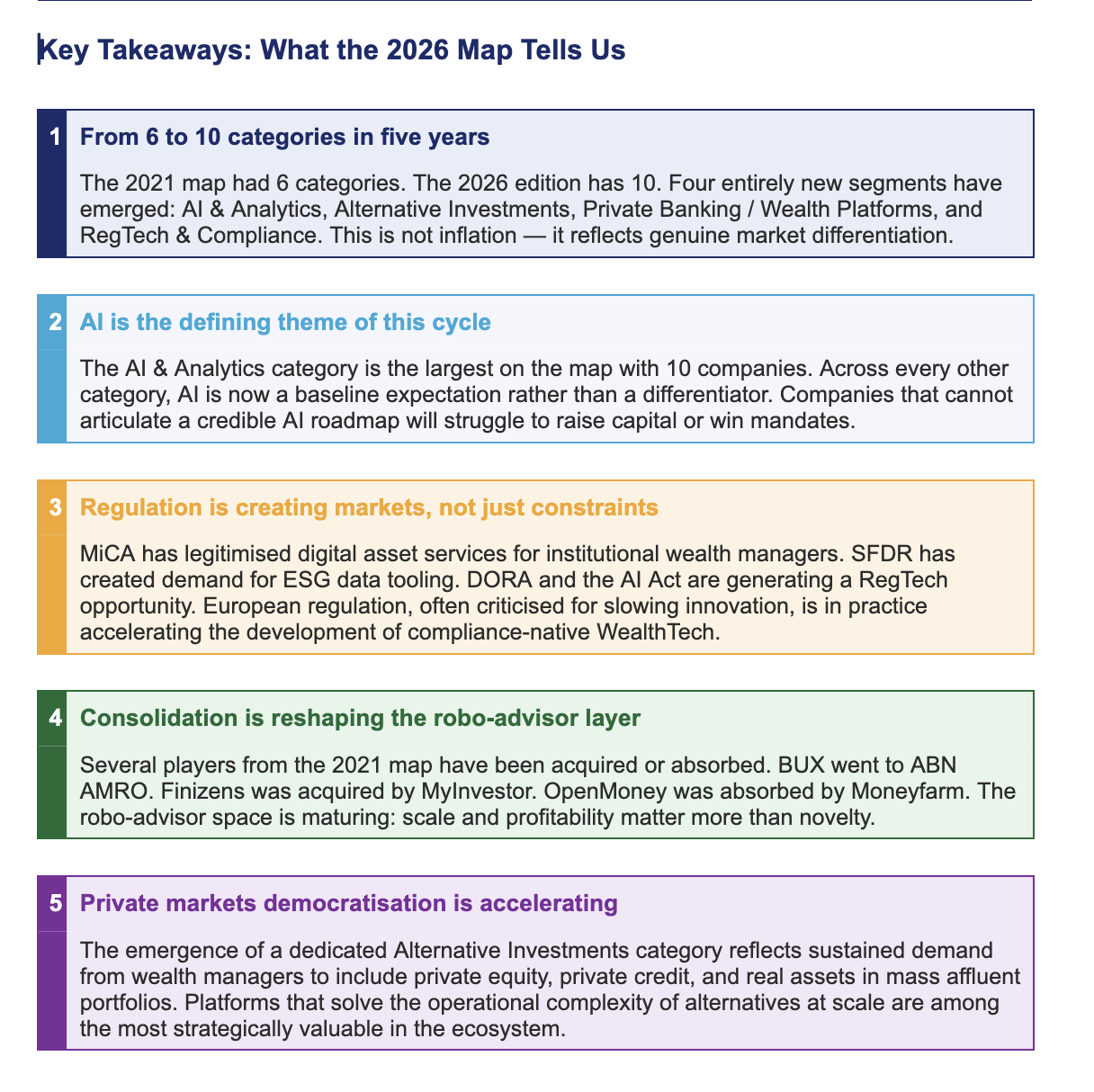

Five years after publishing our first European WealthTech Map, Mandalore Partners releases its 2026 edition. The landscape has changed dramatically. What began as a handful of robo-advisors and portfolio software vendors has evolved into a sophisticated, multi-layered ecosystem spanning artificial intelligence, digital assets, ESG data, and regulatory technology.

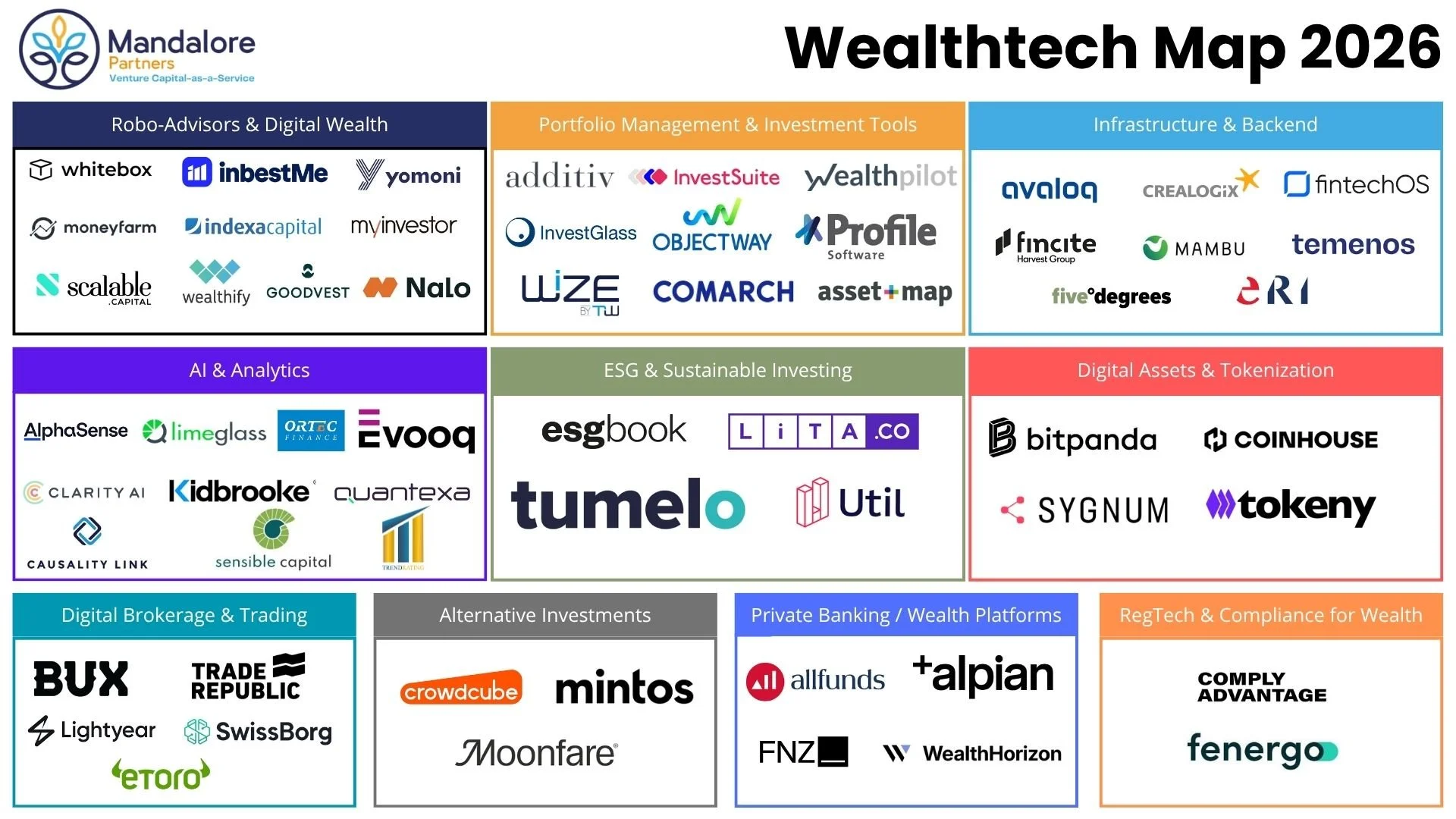

This year's map features 48 companies across 10 distinct categories, reflecting how wealth management technology has matured and specialised across Europe. Here is what the data tells us.

1. Robo-Advisors and Digital Wealth: A Maturing Market

The robo-advisor segment remains one of the most populated on the map, with 10 players including Scalable Capital, Moneyfarm, Indexa Capital, Yomoni, and Nalo. What distinguishes the 2026 cohort from earlier iterations is scale and profitability focus. The era of growth-at-all-costs is over.

• Scalable Capital has crossed the 20 billion euro AUM threshold, confirming its position as the undisputed European leader.

• InbestMe and Indexa Capital anchor the Iberian market with strong organic growth driven by pension automation products.

• Goodvest and Wealthify represent a new generation of purpose-driven robo-advisors embedding ESG at the core of their offering rather than as an add-on.

The presence of MyInvestor, which acquired Finanbest in 2023, illustrates the consolidation wave reshaping this category. Standalone robo-advisors without a differentiated niche or a banking licence will face mounting pressure in the next 24 months.

2. Portfolio Management and Investment Tools: The B2B Engine

With nine companies including Additiv, Objectway, InvestSuite, and Wealthpilot, portfolio management infrastructure remains the connective tissue of European wealth management. These are largely B2B platforms powering the digital transformation of private banks, asset managers, and IFAs.

• Additiv continues to expand its digital finance suite into the Middle East and Asia, using its Swiss base as a regulatory anchor.

• Wealthpilot is gaining ground among German-speaking independent advisors, a market that has historically resisted digitalisation.

• Comarch and Profile Software serve the Eastern European and Mediterranean private banking segments, markets often overlooked by pan-European analysts.

★ Asset-Map stands out as one of the most distinctive tools in this category. Rather than focusing on portfolio performance alone, it maps the full financial picture of a client (assets, liabilities, income streams, insurance coverage) in a single visual.

3. Infrastructure and Backend: The Invisible Foundation

Eight companies form the backbone of the European WealthTech stack. Avaloq and Temenos are the established giants, each processing trillions in assets annually. But the 2026 map reveals a new generation of cloud-native challengers worth watching.

• FintechOS is emerging as the most credible alternative to legacy core banking systems for wealth-adjacent use cases, particularly in Eastern Europe and the UK.

• Mambu has expanded aggressively into wealth management after establishing its footprint in lending and neobanking.

• Fincite acquired by Harvest Group in 2025, now operates as part of a larger French data and technology group, giving it distribution reach it previously lacked.

The presence of Five Degrees and ERI reflects the continued relevance of specialist wealth management core systems, particularly for private banks and family offices that require deep customisation over out-of-the-box standardisation.

4. AI and Analytics: The Fastest-Growing Category

With ten companies, AI and Analytics is the most populated category on the 2026 map and the one that has seen the most new entrants since 2021. This reflects a broader shift: wealth managers are no longer asking whether to adopt AI but how fast they can deploy it.

• AlphaSense has become the de facto standard for investment research intelligence among European asset managers.

• Clarity AI bridges the ESG data and AI analytics worlds, a positioning that makes it relevant across two high-growth categories.

• Quantexa applies network analytics and entity resolution to client intelligence and financial crime detection in wealth management contexts.

• Kidbrooke and Evooq

★ Trendrating is one of the players in this category that engaged directly with our research team for this edition. Their momentum-based rating system scores equities and ETFs on price trend strength and is gaining adoption among European wealth managers who want a systematic, rules-based overlay for portfolio construction without relying solely on traditional fundamental analysis. Their input helped sharpen our understanding of how AI-assisted signal generation is being operationalised at the advisor level, not just in quant funds.

The emergence of Sensible Capital, Causality Link, and Limeglass reflects the depth of specialisation now visible in this category. European wealth management AI is no longer a single use case: it spans research, client profiling, risk analytics, and regulatory reporting.

5. ESG and Sustainable Investing: Small but Strategic

Four companies make up the ESG category: ESGbook, LITA.co, Tumelo, and Util. The relatively small size of this segment belies its strategic importance. ESG data and tooling are increasingly embedded across every other category on the map rather than sitting in isolation.

• Tumelo has built a compelling shareholder engagement product that allows wealth managers to pass voting rights through to end investors, a capability that regulators are beginning to formalise.

• ESGbook provides corporate sustainability data at a granularity that rivals the large incumbent data providers, at a fraction of the cost.

• LITA.co occupies a unique position as a crowdfunding and impact investment platform focused on mission-driven European SMEs.

As SFDR obligations deepen and clients increasingly demand sustainability evidence rather than sustainability claims, the ESG tooling layer will grow in importance and likely in company count by the 2027 edition.

6. Digital Assets and Tokenization: From Experiment to Infrastructure

Four companies form the Digital Assets and Tokenization category: Bitpanda, Coinhouse, Sygnum, and Tokeny. Each takes a meaningfully different approach, reflecting the range of strategies viable in a post-MiCA regulatory environment.

• Bitpanda has evolved from a retail crypto platform into a regulated financial infrastructure provider, now offering its technology to banks and wealth managers.

• Sygnum operates as a fully regulated digital asset bank, licensed in Switzerland and Singapore, serving institutional and private banking clients.

• Tokeny focuses on the tokenisation of real-world assets including private equity, real estate, and structured products, a use case gaining serious institutional traction.

• Coinhouse anchors the French-speaking market with both retail and professional crypto services under French regulatory oversight.

The arrival of MiCA in 2024 has been transformative for this category. European wealth managers who previously avoided digital assets for compliance reasons are now actively evaluating how to incorporate tokenised securities into client portfolios.

7. Digital Brokerage and Trading: Consolidation and Reinvention

Five players populate the brokerage category: BUX, Trade Republic, Lightyear, SwissBorg, and eToro. The story here is one of rapid maturation and strategic repositioning.

• Trade Republic has grown into one of Europe's most significant retail investment platforms, now offering savings products and payment features alongside brokerage.

• eToro completed its long-awaited Nasdaq IPO in 2025, validating the social trading model at scale.

• Lightyear is targeting the pan-European commission-free brokerage space vacated by the acquisition of DEGIRO by flatex.

• SwissBorg bridges the crypto and traditional investment worlds with a focus on yield optimisation for digital assets.

8. Alternative Investments: Opening Private Markets

Three platforms define the alternative investments category: Crowdcube, Mintos, and Moonfare. Together they represent the democratisation of asset classes historically reserved for institutional or ultra-high-net-worth investors.

• Moonfare has built the leading platform for private equity fund access below the institutional minimum, with over 30 funds available to accredited investors.

• Mintos has evolved beyond its peer-to-peer lending origins into a regulated multi-asset alternative investment marketplace.

• Crowdcube remains the dominant UK and European equity crowdfunding platform, connecting growth companies with retail and professional investors.

The inclusion of this category in the 2026 map reflects a structural shift: European wealth managers are under pressure to include alternatives in client portfolios as low interest rate returns on traditional assets compress. Platforms that reduce the operational burden of alternatives allocation will be significant beneficiaries.

9. Private Banking and Wealth Platforms: Digitising the High End

Four companies anchor the private banking and wealth platforms category: Allfunds, Alpian, FNZ, and WealthHorizon. This segment addresses the complexity of serving high-net-worth and ultra-high-net-worth clients at scale.

• Allfunds operates the largest B2B fund distribution network in Europe, connecting over 2,500 fund houses with distributors across 60 countries.

• FNZ provides the end-to-end platform infrastructure behind many of Europe's largest wealth management propositions, processing over 1.5 trillion euros in assets.

• Alpian is building the digital private bank of the future in Switzerland, combining human advisory with a sleek digital interface for clients above 100,000 euros in investable assets.

★ WealthHorizon targets the family office and multi-family office segment with a consolidated portfolio and reporting platform built for multi-asset, multi-currency, multi-entity complexity. WealthHorizon engaged with our research team for this edition, providing direct input on how European family offices are approaching technology consolidation — moving away from fragmented spreadsheet-based reporting toward integrated platforms capable of handling alternatives, direct investments, and cross-border structures in a single view. Their perspective reinforced a clear theme: the family office market in Europe is at an inflection point, and the demand for institutional-grade tooling at sub-institutional scale has never been stronger.

10. RegTech and Compliance for Wealth: A New Category for 2026

The most significant addition to the 2026 map relative to previous editions is the RegTech and Compliance for Wealth category, featuring ComplyAdvantage and Fenergo. Its emergence as a standalone segment reflects how compliance has moved from a back-office cost centre to a front-office strategic concern.

• ComplyAdvantage provides AI-driven AML, KYC, and sanctions screening, increasingly deployed by wealth managers facing tighter regulatory scrutiny.

• Fenergo specialises in client lifecycle management and regulatory onboarding, reducing the time and cost of bringing high-net-worth clients onto platform.

As DORA, MiCA, SFDR, and the AI Act create overlapping compliance obligations for European wealth managers, the demand for purpose-built RegTech tooling will only accelerate. We expect this category to double in company count by 2027.

About Mandalore Partners

Mandalore Partners is a Venture Capital-as-a-Service firm specialising in FinTech, InsurTech, and WealthTech. We advise corporate investors and institutional LPs on their innovation strategy and help them identify, evaluate, and invest in the most relevant technology companies across Europe.

The European WealthTech Map 2026 is a non-exhaustive selection based on our proprietary research and deal flow. For further information or to discuss a company's inclusion in future editions, contact alice@mandalorepartners.com.