En résumé : un AIR Venture Program est bien plus qu'un budget R&D orienté IA. C'est une architecture d'investissement structurée qui combine capital, partenariats commerciaux et gouvernance pour capter les meilleures startups IA avant la concurrence. Ce guide détaille comment le structurer, le piloter et le mesurer.

Introduction : pourquoi les corporates ne peuvent plus ignorer les startups IA

L'intelligence artificielle n'est plus un sujet de futur — c'est une réalité compétitive du présent. En 2026, les entreprises qui n'ont pas encore structuré une approche d'investissement ou de partenariat avec les startups IA les plus prometteuses accusent déjà un retard stratégique mesurable.

Mais investir dans des startups À ne s'improvise pas. Les erreurs les plus fréquentes observées par Mandalore Partners dans les programmes corporate IA incluent : des investissements dispersés sans thèse cohérente, des pilotes qui ne passent pas à l'échelle faute de gouvernance, et des startups sélectionnées sur des critères technologiques sans validation du product-market fit.

Ce guide détaille comment les corporates les plus avancés structurent leur AI Venture Program en 2026 — de la définition de la thèse à la mesure des KPIs, en passant par les modèles de partenariat et les structures d'investissement.

1. Qu'est-ce qu'un AI Venture Program ?

Un AIR Venture Program est une initiative structurée via laquelle une organisation corporate investit dans des startups IA alignées avec ses objectifs stratégiques, ou noue des partenariats commerciaux approfondis avec elles, dans le but de transformer ses opérations, créer de nouveaux produits ou accélérer sa compétitivité sectorielle.

Un AIR Venture Program efficace repose sur trois piliers complémentaires :

2. Pourquoi 2026 est le moment d'agir

La consolidation du marché À créer des fenêtres d'entrée

Après l'euphorie de 2021-2022 et la correction de 2023, le marché des startups IA a opéré une sélection naturelle. Les acteurs qui subsistent en 2026 présentent des métriques de croissance robustes, des clients payants et une voie vers la rentabilité. Les valorisations, bien qu'en reprise, restent plus raisonnables qu'en 2021 — créant des points d'entrée attractifs pour les investisseurs stratégiques.

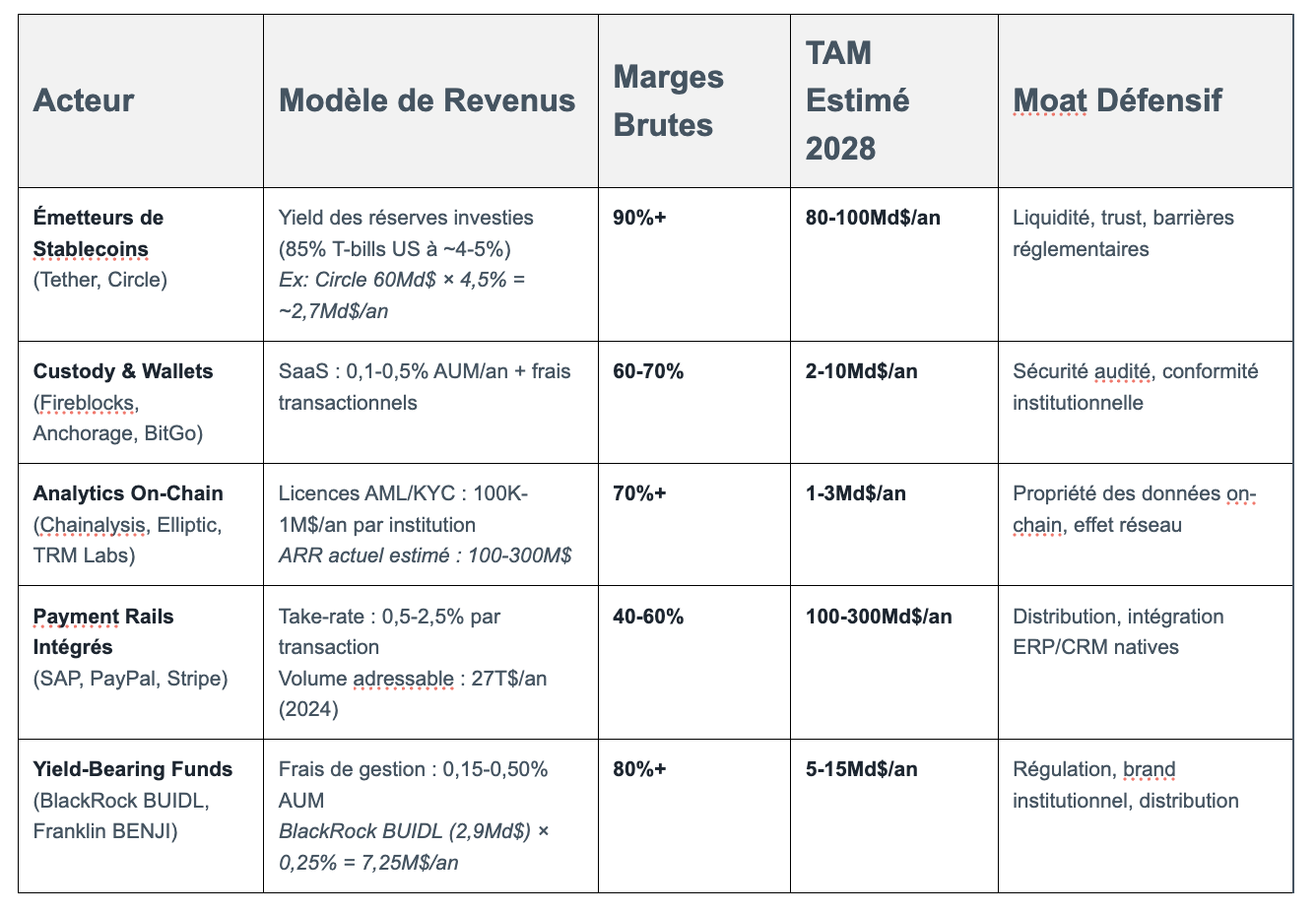

L'IA generative se verticalise secteur par secteur

En 2026, l'IA générative n'est plus un phénomène horizontal : elle se verticalise. Des start ups développent des LMS et des agents IA spécialisés pour l'assurance (automatisation des sinistres), la finance (modélisation du risque, détection de fraude), l'industrie (maintenance prédictive, contrôle qualité) et la santé (aide au diagnostic, découverte de molécules). Ces verticales correspondent précisément aux secteurs de la stratégie 4i de Mandalore Partners.

La concurrence pour les meilleures startups IA s'intensifie

Les fonds VC tier-1 européens (Balderton, Northzone, Speed Invest, Partech) et américains sont déjà positionnés sur les meilleurs dossiers IA. Les corporates qui n'ont pas encore structuré un programme d'investissement risquent d'être exclus des tours les plus attractifs — ou d'y accéder uniquement a des conditions moins favorables.

Chiffres clés IA Venture Europe 2026

Investissements VC IA en Europe : +42 % en 2025 vs 2024 (Source : Dealroom)

Nombre de startups IA européennes actives : plus de 4 200

Top 3 secteurs IA les plus financés : HealthTech, FinTech, Industry Tech

Valorisation médiane Série A IA Europe : 28 M€ (vs 18 M€ en 2023)

3. Les 6 étapes pour structurer votre AI Venture Program

Etape 1 — Définir votre thèse IA

Avant d'investir le moindre euro, votre organisation doit répondre à trois questions fondamentales :

Quels sont vos défis opérationnels les plus urgents que l'IA peut résoudre ?

Ou l'IA peut-elle créer un avantage compétitif durable dans votre secteur ?

Quels types de startups cherchez-vous : partenaires commerciaux, fournisseurs technologiques ou investissements purs ?

La thèse doit être suffisamment précise pour guider la sélection (ex. : "startups IA B2B améliorant la souscription ou le claims en assurance IARD en Europe") sans être si restrictive qu'elle exclut les opportunités adjacentes les plus prometteuses.

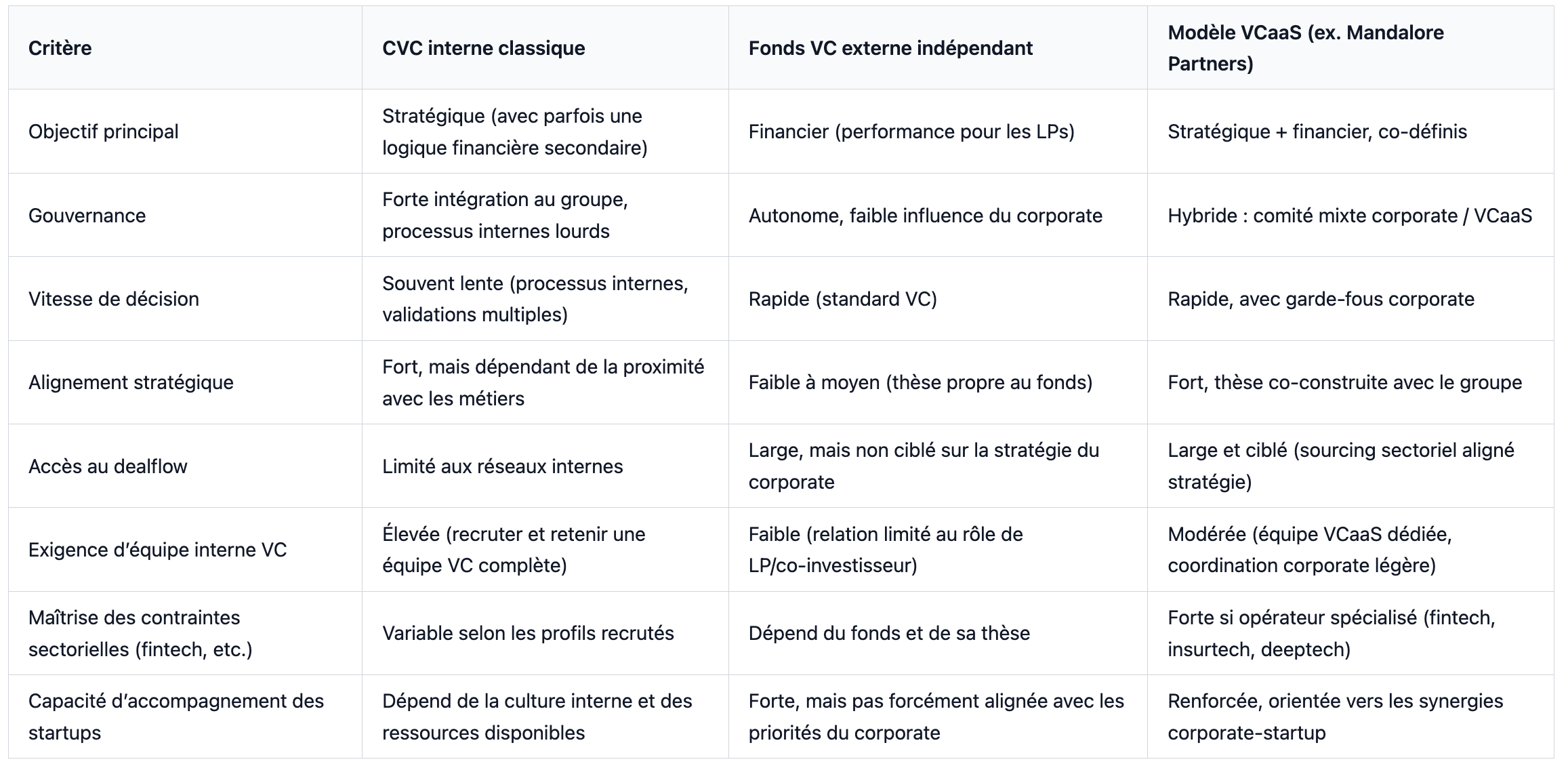

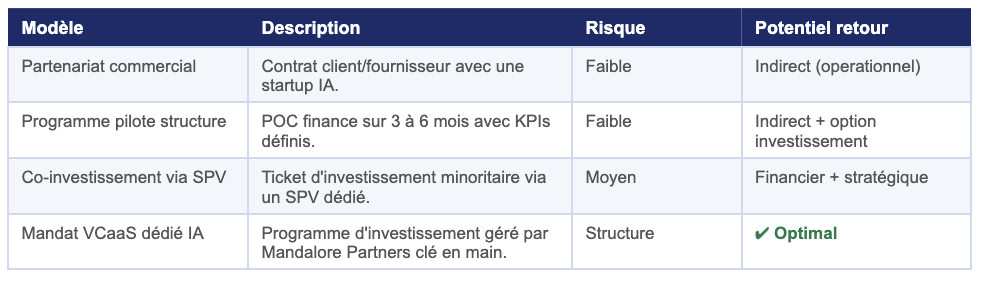

Etape 2 — Choisir le bon modèle d'engagement

Il existe quatre modèles d'engagement possibles avec les startups IA, par ordre croissant d'intensité :

Etape 3 — Définir le budget et la structure

Les budgets des AI Venture Programs varient considérablement selon l'ambition et la taille de l'organisation. Voici les fourchettes observées par Mandalore Partners sur ses mandats européens :

Programme exploration (moins de 2 M€/an) : 3 à 5 partenariats commerciaux ou pilotes, sans investissement en capital. Idéal pour tester la démarche.

Programme d'investissement cible (2 a 10 M€/an) : 2 à 5 investissements directs via SPV ou fonds dédié. Recommandé pour les corporates avec une thèse claire.

Programme institutionnel (10 à 50 M€/an) : fonds dédié géré en VCaaS ou en CVC semi-interne, avec un portefeuille de 10 à 20 startups sur un horizon de 7 ans.

Etape 4 — Sourcer les meilleures startups IA

Le deal flow est l'enjeu central de tout programme d'investissement startup. Les sources les plus efficaces pour les AI Venture Programs en 2026 :

Réseaux VC spécialisés : les fonds qui investissent déjà dans votre verticale sont les meilleurs prescripteurs.

Accélérateurs sectoriels : Station F, Entrepreneur First, The Family, ou les accélérateurs corporate (AXA Next, BNP Paribas Plug and Play).

Évenements IA : VivaTech, AI Summit London, Web Summit, NeurIPS.

Partenaire VCaaS : la solution la plus efficace pour un dealflow propriétaire immédiat, présélectionné et aligne sur votre thèse — c'est la proposition de valeur centrale de Mandalore Partners.

Etape 5 — Structurer la due diligence IA

La due diligence d'une startup IA necessite une grille d'évaluation adaptée, en complément des critères VC classiques :

Qualité des données : l'IA est aussi bonne que ses données. Évaluer la propriété, la qualité et l'exclusivité des datasets utilisés.

Défendabilité technologique : est-ce un wrapper de GPT-4 ou une architecture propriétaire ? Quelle est la barrière à l'entrée réelle ?

Réglementation IA Act : conformité au règlement européen sur l'IA, en vigueur depuis 2024. Particulièrement critique pour les applications en santé, assurance et finance.

Scalabilité du modèle économique : les coûts d'inférence (GPU, cloud) sont-ils absorbables à l'échelle ? Quel est le chemin vers la rentabilité ?

Equipe : expertise en ML/ML Ops, capacité à recruter des AI engineers dans un marché très concurrentiel.

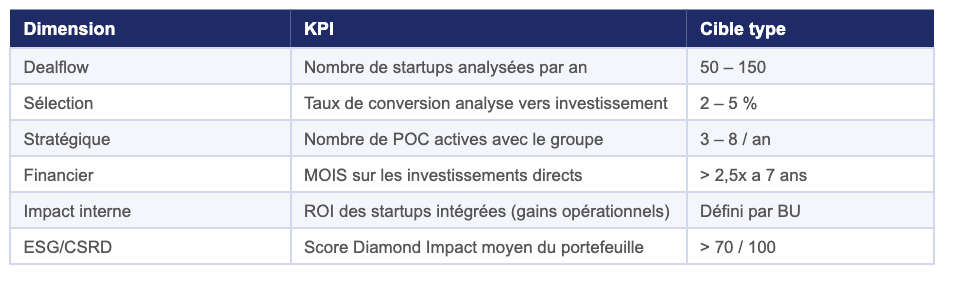

Etape 6 — Définir les KPIs et le suivi de portefeuille

Un AIR Venture Program sans KPIs mesurables est voué à être abandonné au premier changement de direction. Les métriques recommandées par Mandalore Partners :

4. Les 5 erreurs les plus fréquentes dans les AI Venture Programs

Erreur 1 — Investir sans these définie

Beaucoup de corporates commencent par investir dans des startups IA "intéressantes" sans cadre stratégique. Résultat : un portefeuille incohérent, sans synergies, et des LP internes qui questionnent la valeur ajoutée du programme.

Erreur 2 — Confondre POC et partenariat stratégique

Multiplier les POC sans processus de passage à l'échelle est une erreur classique. Chaque PC doit être conçu avec des critères de succès prédéfinis et un chemin clair vers l'intégration ou l'abandon.

Erreur 3 — Sous-estimer le temps de due diligence IA

Évaluer une startup IA prend 2 à 3 fois plus de temps qu'une startup classique en raison de la complexité technique et réglementaire. Ne pas prévoir les ressources adéquates conduit à des décisions précipitées.

Erreur 4 — Négliger le reporting SFDR/CSRD

Les investisseurs institutionnels et les directions financières exigent de plus en plus un reporting ESG sur les allocations venture. Un programme sans cadre de mesure impact crée des frictions avec la gouvernance interne.

Erreur 5 — Vouloir tout internaliser trop vite

La tentation de "monter un CVC en interne" après quelques investissements réussis est forte, mais prématurée. Construire une équipe VC crédible prend 3 à 5 ans minimum. Le VCAS permet de capitaliser sur l'expertise existante tout en gardant le contrôle stratégique.

5. Le programme AI Venture de Mandalore Partners

Mandalore Partners propose un mandat VCaaS dédié aux programmes d'investissement IA, couvrant l'intégralité du cycle :

Définition de la thèse IA en co-construction avec votre équipe (1 à 2 ateliers de cadrage)

Sourcing propriétaire via notre réseau européen et international de plus de 2 000 startups actives

Due diligence renforcee IA : technique, réglementaire (IA Act), financière et ESG

Structuration adaptée au mandat : SPV dédié, co-investissement, fonds theme

Suivi de portefeuille actif : gouvernance, accompagnement commercial, ouverture réseau

Reporting Diamond Impact Scoring : aligne CSRD et SFDR Article 8, compatible avec les exigences de votre comité d'investissement

Notre focus sectoriel 4i (InsurTech, Invest Tech, Impact Tech, Industry Tech) nous positionne sur les startups IA les plus pertinentes pour les corporates du secteur financier et industriel — avec un deal flow propriétaire impossible à répliquer sans des annees de présence dans l'écosystème.

Conclusion

Structurer un AIR Venture Program n'est plus une question de "si" mais de "comment" et "à quel rythme". Les organisations qui agiront en 2026 bénéficieront d'un avantage de premier entrant sur les meilleures startups IA de leur secteur, des valorisations encore raisonnables par rapport aux cycles précédents, et d'un alignement optimal avec les transformations opérationnelles en cours.

Le modèle VCaaS de Mandalore Partners est précisément conçu pour permettre à des organisations ambitieuses de démarrer en quelques semaines, avec une discipline institutionnelle et un reporting alignée sur les exigences de leur gouvernance.

Vous souhaitez lancer votre AI Venture Program ?

Decouvrir notre programme --> mandalorepartners.com/ai-venture-program

Rencontrer notre equipe --> mandalorepartners.com/meet

En savoir plus sur le VCaaS --> mandalorepartners.com/venture-capital-as-a-service