Why this conference is a signal worth reading

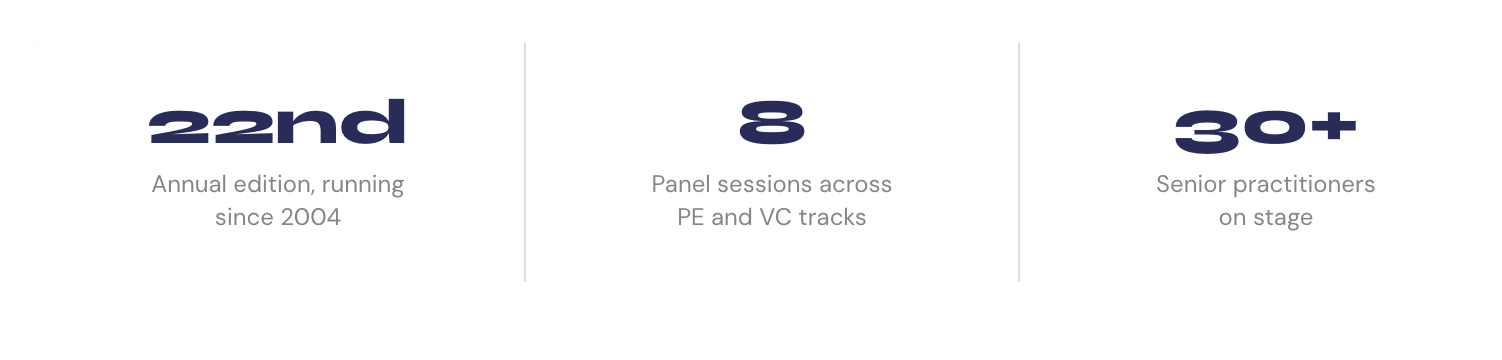

The INSEAD Private Equity Club (IPEC) has been running this conference for 22 years. What makes it unusual is its audience mix: LP allocators, GP principals, investment bankers, and a dense layer of INSEAD alumni now running funds or managing assets for large institutions. It is not a marketing event. The Chatham House rule keeps it honest.

This year's theme — implicit rather than stated — was recalibration. Not crisis. Not euphoria. Something in between: a market that has processed the rate shock, survived the distribution drought, and is now sorting out which managers, strategies, and asset classes deserve capital at a higher cost of it.

Eight sessions ran across two tracks: a Plenary room that opened with LP dynamics and closed with infrastructure, and parallel PE/VC breakouts that ran from early afternoon. I took notes across all of them. What follows is my read of the room — the tensions, the surprising consensuses, and the questions the industry hasn't answered yet.

Session 01 · Plenary

Capital Allocation: Earning the Re-Up in a More Selective Market

The opening panel set the table for the whole day. The question wasn't whether LPs are reducing allocations to private markets — they're not, broadly — but rather who gets the capital when denominator effects, liquidity constraints, and rising rates all tighten the filter simultaneously.

Two things stood out from this session. First, the re-up conversation has fundamentally changed. In the 2021 vintage environment, LPs re-upped based on brand, relationships, and paper markups. Today, they want distributions. Not just multiples — actual cash returned. Managers who haven't returned capital face a harder conversation at Fund IV or V, regardless of the unrealized portfolio quality narrative they put forward.

Second, Europe is gaining allocation share against North America in a real way. This is a genuine structural shift, not a temporary swing. The drivers: lower entry multiples, less crowded deal markets in most sectors, more attractive macro relative to US stretched valuations, and — increasingly — a currency argument that institutional investors in the US are starting to listen to. European GPs who can articulate a clear differentiated edge are finding LP conversations markedly easier than three years ago.

"The bar for a re-up used to be 'do I trust this team?' Today it's: 'has this team actually returned my capital?' Trust is necessary. It is no longer sufficient."

Captured under Chatham House rules · Capital Allocation panel

The third thread in this conversation was the fragmentation of LP types. Sovereign wealth funds, US endowments, European insurers, and family offices are all moving differently. The SWF and endowment crowd is consolidating GP relationships — fewer managers, larger tickets, deeper partnerships. European insurers are the most constrained by Solvency II capital charges and are looking for structures that minimize balance sheet impact. Family offices are the most opportunistic and the fastest to act, but the least predictable on follow-on.

For anyone raising or planning to raise a fund in the next 18 months: the message was direct. Focus on your distribution story before your valuation story. Know your LP type and structure accordingly. And if you're European, lead with your European-ness — it is an asset right now, not a handicap.

Session 02 · Plenary

Secondaries: Governance, Conflicts, and the Price of Liquidity

If the first session was about LPs making choices, this one was about GPs engineering liquidity when the natural exit market isn't cooperating. Secondaries have gone from niche tool to structural feature of private markets — and the panel made clear this is not a temporary workaround but a permanent evolution.

The secondary market has roughly tripled in volume in the past five years. What changed: the rise of GP-led continuation vehicles as the dominant deal structure. In a GP-led deal, the original GP offers existing LPs a liquidity option while rolling top-performing assets into a new vehicle. It sounds clean. The room's discussion was frank about the tension: the GP simultaneously plays advisor to selling LPs and buyer of the assets being sold. That is a real conflict, and the industry's self-regulatory response has been uneven.

"GP-led is not inherently conflicted. It is inherently a structure where the conflict has to be managed explicitly, transparently, and with third-party validation. When that discipline holds, it works. When it doesn't, it's a transfer from LP to GP."

Captured under Chatham House rules · Secondaries panel

The pricing discussion was nuanced. Secondary discounts to NAV have compressed significantly from the 30-40% levels seen in 2022-2023. In quality assets with strong cash flows and credible GP track records, the market is trading close to or at NAV — sometimes above in competitive processes. The implication: the easy vintage of buying distressed secondaries at massive discounts is largely over. Future returns in secondaries will require more genuine asset selection skill, not just price arbitrage.

One practical angle for the audience: for corporate LPs with illiquid PE allocations, the secondary market is increasingly a viable exit tool — not a last resort. The liquidity premium is much lower than it was. GPs with well-performing portfolios should be proactively educating their LPs on this option rather than waiting for LPs to ask.

Session 03 · Plenary

The Long Game: How La Caisse Underwrites European Private Equity

La Caisse de dépôt et placement du Québec manages over $450bn in assets and is one of the most sophisticated institutional investors in European private equity. This session was genuinely illuminating because it offered a long-horizon LP's unfiltered view of the current cycle — not the polished version that ends up in LP communications, but the practitioner's read.

The core message: conviction is now the differentiating currency. In a more selective capital allocation environment, La Caisse is choosing to concentrate relationships with fewer GPs where they have deep conviction about the team, the thesis, and the alignment. The era of allocating broadly across a large roster of GPs as a diversification strategy is over for sophisticated allocators. Portfolio concentration with high-conviction managers is the direction.

On the question of when to sell — something LPs rarely discuss publicly — the session was surprisingly candid. The classic LP posture is to hold through the fund life and accept whatever exit the GP engineers. La Caisse's approach is more active: they model exit scenarios at the GP level and engage proactively on exit timing when they believe a GP is holding too long into a deteriorating strategic window. This is a real shift from passive LP to something closer to an engaged strategic co-investor.

GP discipline came up repeatedly. What does discipline mean right now? Not deploying capital at peak prices just to put money to work. The vintage problem is real: funds raised in 2021-2022 at peak entry multiples are sitting on portfolios that will be very hard to exit at the marks. GPs who didn't invest during that window are well-positioned for the current deployment environment. That differentiation is increasingly visible to sophisticated LPs.

Key LP signal

Sophisticated allocators like La Caisse are consolidating around fewer, higher-conviction GP relationships. If you're a first or second-time fund manager without a demonstrable edge, the access to these LPs is closing. The window for brand-new entrants to access institutional capital is narrower than it was — and it requires a much stronger proof-of-concept.

Session 04 · PE Track

Private Equity at a Turning Point

The afternoon PE track opened with the most direct conversation of the day about the reality of buying and building companies in 2026. The panel — KKR, PAI, and Astorg — represent a useful cross-section: global mega-fund, European large-cap specialist, and European mid-market specialist. Their views converged more than they diverged, which itself is a signal.

The deployment dynamics have normalized. After the near-freeze of 2023, deal activity in European PE has recovered — particularly in the mid-market, where sellers have become more realistic on valuation. The bid-ask spread has compressed meaningfully, which is a necessary condition for deal flow. The strategic rationale for many transactions has also shifted: less multiple expansion thesis, more operational transformation thesis. GPs are underwriting to operational improvements, margin expansion, and geographic expansion rather than betting on re-rating.

Operational excellence came up repeatedly as the defining capability gap between GPs. The days when financial engineering — leverage optimization, cost cuts, multiple arbitrage — could drive the bulk of value creation are structurally over in a higher rate environment. What replaces it: genuine operational transformation capacity, which means embedded operational teams, proprietary value creation playbooks, and the ability to attract C-suite executives to portfolio companies. This is harder to build than a financial model. Firms that have invested in this capability for years are now seeing the payoff.

Session 05 · VC Track

AI and Beyond: Where Real Value Is Emerging Across Tech

This was the session the room was most eager for — and it largely delivered. Three experienced European VC investors, no slides, talking candidly about how the AI wave is sorting itself out from an investment perspective.

The starting point: the AI investment landscape in Europe is not the same as in the US. There is no European OpenAI, no European Anthropic. The infrastructure layer — foundation model training, data center buildout, GPU economics — is largely playing out in the US and in a handful of hyperscaler-adjacent contexts. Where European VC can genuinely win is in AI application to vertical sectors: insurance, healthcare, legal, logistics, manufacturing, and financial services. Not the picks-and-shovels game — the specific application layer where domain knowledge and regulatory fluency create defensible positions.

"Everyone is building on top of GPT-4 or Claude. That is not a moat. The moat is the data, the domain knowledge, the regulatory relationship, and the customer trust that a pure software company cannot replicate. Europe has those in abundance — in insurance, healthcare, industrial sectors."

Captured under Chatham House rules · AI/Tech VC panel

The panel was notably skeptical of "AI wrapper" companies — tools that simply put a chat interface on top of a foundation model without proprietary data or genuine workflow integration. The filter question from investors has shifted: not "does this use AI?" but "what happens to this company when GPT-6 ships and makes this specific capability commodity?" Companies that can't answer that question don't get funded in the current environment.

What does pass that filter? Companies with a proprietary data flywheel — where using the product generates data that trains better models that attracts more users. Healthcare diagnostics on rare disease data. Insurance underwriting on unique actuarial datasets. Legal document analysis on specialized case law. These are compound advantages that are genuinely hard to replicate, and European startups in these verticals are meaningfully ahead of US equivalents in several regulatory jurisdictions.

On valuations: the AI premium has compressed from the 2023-2024 highs. Seed-stage AI companies are still getting aggressive terms, but Series A and B rounds have normalized significantly. Investors now expect revenue traction, not just demo video traction. This is healthy.

Session 06 · PE Track

Private Credit in Europe: Built for Growth, Tested by the Cycle

Private credit has been the story of European private markets for the past three years. The capital has flowed in, spreads have compressed, and the cycle is now stress-testing whether the underwriting was disciplined or just yield-chasing dressed up in covenant language.

The panel was honest about the bifurcation in the market. Quality direct lending — first lien, core middle market, covenant-heavy, well-diversified portfolios — is performing as expected. The stress is showing up at the edges: over-leveraged LBOs that were financed at peak valuations with loose covenants, CLO tranches with concentrated exposures, and some sector-specific stress (retail, commercial real estate adjacents, certain tech names). These are manageable at the portfolio level but are visible in loss reserves.

The most interesting structural theme: European banks are not coming back as the primary source of mid-market credit. Basel IV capital requirements, regulatory pressure on leveraged lending, and ongoing balance sheet management by European banks mean the structural gap that private credit filled from 2015 onwards is permanent. The market is not overcrowded — it is meeting genuine demand that will not disappear.

One tension surfaced clearly: covenant-lite structures have arrived in Europe, imported from the US leveraged loan market through large sponsor transactions. The panel had mixed views. Some see it as market maturation. Others see it as the precise mechanism through which the next credit cycle casualty will emerge. Watch this space.

From a corporate LP perspective — particularly insurers with Solvency II frameworks — private credit offers something genuinely useful: duration-matched cash flows with spread pickup over public bonds. The regulatory treatment under Solvency II for qualifying private credit instruments has improved, and several European insurers on the room are actively building allocations. Generali's presence on this panel was telling.

Session 07 · VC Track

Investing for Impact: Climate, Health, and the Next Frontiers of Venture

The impact and sustainability session could have been — and in past years occasionally was — a performance of values rather than a serious investment conversation. This year's version avoided that trap. The panel took a notably rigorous stance: impact investing either delivers financial returns or it doesn't get called impact investing. The era of accepting concessionary returns in exchange for mission alignment is over in the institutional LP community.

What that means in practice: climate and health VCs are now building genuine dual-return theses where the environmental or social outcome is embedded in the business model itself, not layered on top. The strongest examples are in insurance-linked climate products (parametric climate risk, cat bond structures), precision medicine where the health outcome drives the commercial outcome, and industrial decarbonization where the carbon cost saving is the P&L upside.

Extantia's framework was particularly sharp: they only invest in companies where the climate tech is also the most economically efficient solution — not a subsidy-dependent alternative. If the tech only works with carbon pricing at €150/tonne, it's not investable yet. If it works at €50, it is.

Impact rigor is now a GP differentiation story, not just a regulatory compliance story — LPs are scrutinizing impact claims like they scrutinize financial claims

The insurance industry is the largest underwriter of climate risk globally and therefore the most natural corporate partner for climate-tech startups with parametric or risk-transfer components

Health impact investing is bifurcating: real biotech (long-horizon, science-driven) and digital health (faster, higher iteration rate) require very different fund structures

Blended finance structures — concessional capital from development banks layered with commercial VC — are becoming mainstream for climate-adaptation plays in emerging markets

Sessions 08 & 09 · PE + VC Track

Infrastructure & Venture Exits: The Two Longest Roads

Infrastructure: The Buildout is Real, the Capital Discipline is Uneven

European infrastructure is in the middle of a genuine supercycle — energy transition, digital infrastructure (data centers, fiber, towers), and transport decarbonization are all creating large-scale capital deployment opportunities. The panel was bullish on the structural opportunity and more measured on execution risk.

The speed-to-power problem dominated the energy transition discussion. Europe's electricity grid cannot absorb the renewable capacity being built fast enough. Interconnection queues are years long in most markets. This is not just a planning problem — it is a fundamental capital allocation risk for new renewable assets. Projects that can secure grid connection have a significant competitive advantage. Projects underwriting against speculative grid access are financing delays and write-downs.

Data centers are the headline story, and the panel's view was nuanced: data center demand is real and structural, but the GP edge is in the details of site selection, power procurement, and cooling infrastructure — not just in signing a hyperscaler anchor tenant. Commoditized data center platforms without differentiated power access will face margin compression.

Venture Exits: Patience Required, Innovation in Structure

The VC exits session was the most candid conversation of the day. The European VC market has not solved its exit problem. IPO windows are episodic, strategic acquirers are selective, and the secondary market for late-stage private shares is thinner than in the US. The result: hold periods have extended from the classic 7-year fund life to 10-12 years for many assets, and funds are exploring structural innovations to manage the mismatch.

G Squared's role — providing secondary liquidity to startup employees and early investors before formal exit — generated a revealing discussion. The demand for this kind of structured liquidity is substantial. Founders who have built companies for 8-10 years, early employees with paper gains but no cash, early angels looking to rebalance — all are customers for secondary liquidity services that the European market is still under-serving.

Probabl's CEO brought a founder's perspective: the pressure to exit is often misaligned with the business's optimal scaling trajectory. The best outcomes require patient capital that can hold through multiple market cycles — and European venture funds with 10-year lives and limited flexibility are not always the right structure for category-creating companies.

Perspective

What This Means from a CVCaaS Angle

I attend this conference every year because it's one of the clearest mirrors for the market dynamics that shape our work at Mandalore Partners. We operate at the intersection of corporate LPs and the venture ecosystem — which means the signals from both the LP allocation panel and the VC exit panel are directly relevant to how we structure programs and advise corporate clients.

Three signals from today that I'm taking back to the office:

1. The LP sophistication bar is rising — and that's good for specialized structures

Corporate LPs — insurers, mutuals, banks — are being pushed by their institutional peers to think more rigorously about private markets allocation. The message from La Caisse's session, translated to the corporate LP context: broad allocation to many managers doesn't work at scale. A structured CVC program with a clear sector thesis, a defined role in the deal flow ecosystem, and a professional management model delivers better outcomes than an ad-hoc portfolio of minority PE bets. This is the argument at the heart of what we build.

2. AI applied to insurance and financial services is the European VC opportunity

The AI/Tech panel's consensus — European VCs win in vertical application, not foundation model infrastructure — maps directly to our InsurTech thesis. The most durable AI companies in insurance will be built by teams that combine machine learning capabilities with deep regulatory knowledge, proprietary actuarial data, and distribution relationships that require years to build. These are companies that need a strategic corporate partner as much as they need a financial investor. That is precisely where CVC-as-a-Service adds value that pure financial VC cannot.

3. The private credit opportunity for European insurers is structural, not tactical

Several of the corporate LPs we work with are in the insurance sector. The private credit session confirmed what we're hearing in conversations: well-structured private credit allocation is becoming a standard component of European insurer investment portfolios, driven by Solvency II optimization, liability duration matching, and spread pickup over public bonds. For insurers without the internal infrastructure to source and underwrite private credit directly, a managed program with an aligned GP is the answer. There's a product development opportunity here that we're actively exploring.

Across all sessions, the day reinforced a single theme: private markets are maturing from a relationship-driven cottage industry to a professionalized institutional asset class. The players who win in that transition are those who can combine institutional discipline with genuine differentiation — in sourcing, operations, governance, or sector knowledge. That transition is our strategic moment.

The 22nd INSEAD PE & VC Conference confirmed what the data has been suggesting: European private markets have absorbed the rate cycle, are normalizing deal activity, and are entering a phase where differentiation — not beta — drives outperformance. The winning themes are clear: operational PE over financial engineering, vertical AI over infrastructure hype, rigorous impact over performative ESG, disciplined credit over covenant-lite chasing.

For corporate LPs sitting on the sidelines of venture capital, the message is equally clear: the structural case for private markets exposure is stronger than it was in 2021, the entry points are better, and the infrastructure to participate without building an internal team from scratch exists. Waiting for perfect conditions is itself a strategic choice — and not necessarily the right one.