EXECUTIVE SUMMARY / OVERVIEW

Les CGP ont su contenir l’inquiétude de leurs clients en profitant de la période de confinement pour mieux les accompagner, mais aussi pour innover et digitaliser leurs cabinets. Les clients se sont montrés plus attentifs aux risques et aux placements responsables et produits de prévoyance retraite. Ils envisagent l’avenir comme étant plus digital et responsable, sans compromettre la rentabilité de leurs investissements ni la personnalisation des services. Dans le monde d’après qui se dessine, la relation client, l’exercice quotidien plus digitalisé mais aussi le renouvellement des générations vont compter tout autant que le devoir de conseil des CGP.

1 – USER

Une sensibilité à l’investissement responsable, mais pas au prix de la rentabilité

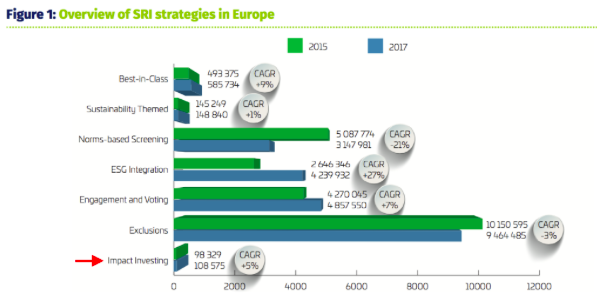

On observe une sensibilité accrue des clients aux critères ISR (Investissement Socialement Responsable).

46 % des professionnels de la gestion de patrimoine s’attendent à voir leurs clients prêter une attention de plus en plus grande à cette dimension responsable dans le choix de leur assurance-vie, et dans la diversification de leurs placements selon le baromètre Cardif BNP Paribas [1].

L’enquête d’Aprédia « Covid-19 : comment les CGP gèrent la crise ? », relève que « l’investissement au travers des produits ISR figure, selon les CGP, parmi les marchés d’avenir » [5].

Une étude d’EY sur des investisseurs canadiens révèle que, si 73 % des répondants ont des objectifs de développement durable (essentiellement axés sur l’environnement), environ la moitié déclarent que leurs conseillers n’y sont pas sensibles. Il y a là une demande à combler [6].

Cette demande des clients se retrouve donc dans l’offre :

Environ 40% des nouveaux fonds créés en 2020 étaient des fonds responsables [5].

L’industrie des fonds immobiliers s’est elle aussi dotée d’un label ISR [5].

La loi Pacte a aidé dans ce sens, son article 72 imposant que les contrats d’assurance vie multi-support conclus à partir du 1er janvier 2020 fassent référence à au moins un fonds labellisé Solidaire, Greenfin, ou Investissement socialement responsable (ISR).

Cependant, si les clients veulent donner du sens à leur épargne, pour la plupart cela ne se fera pas au détriment de la rentabilité de leur investissement [6].

Vers plus de diversification

La crise nous a permis d’observer que, plus sensibles au risque, les clients recherchent une diversification accrue de leurs investissements (61% des clients ont opté pour la diversification de leurs avoirs durant la crise sanitaire) [1].

Les investisseurs souhaitent avoir accès à une plus grande gamme de produits. Actuellement, ils utilisent en moyenne 4,1 produits de placement, mais ils s’attendent à adopter une moyenne de 5,5 produits d’ici 2024 [6].

De leur côté, les CGP veulent plus de diversification au sein des contrats d’assurance vie et scrutent les nouvelles opportunités, notamment dans l’immobilier (SCPI, SCI, OPCI) et les produits alternatifs [5].

Les investisseurs veulent plus de personnalisation

Au-delà du conseil financier, les investisseurs souhaitent un accompagnement plus personnalisé de leurs conseillers en gestion de patrimoine. La tendance est vers un véritable accompagnement durable dans chaque moment de vie [3]. Cette tendance à la personnalisation répond aussi à une démographie des clients changeante.

Les CGP font face à une population de plus en plus fragmentée : célibataires, millennials, familles monoparentales… et la personnalisation est de mise pour bien répondre à chaque attente. L’enjeu à l’avenir est la relation humaine et le contact direct avec les investisseurs, pour personnaliser les conseils et l’accompagnement [4].

2 – TECH

La digitalisation, accélérée par la crise, pour un modèle hybride à l’avenir

Pendant la crise, 85% des CGP ont opté pour des outils digitaux donnés par leurs fournisseurs pour la gestion des dossiers et 82% ont travaillé en télétravail. A l’avenir, plus des trois quarts des CGP anticipent un renforcement des usages digitaux par leurs clients après cette crise, que ce soit pour effectuer des démarches administratives, gérer l’après-vente ou simplement communiquer [1].

Les CGP ont dû adapter leurs modes de communication pour accompagner directement avec le client : 3 CGP sur 4 ont ainsi adapté leurs modes de communication (visioconférence, téléphone, tchat) [1].

Cette digitalisation, vue dans un premier temps comme un risque pour le métier, permet aujourd’hui aux CGP de se délester des tâches les plus fastidieuses pour apporter de nouveaux services à leurs clients, et se concentrer sur la partie conseil de leur métier [3].

Cette digitalisation permet aussi d’améliorer la personnalisation du service, grâce au partage de données [6]. L’intelligence artificielle, quant à elle, représente une opportunité pour les CGP pour l’analyse des allocations d’actifs en fonction des profils de risque par exemple (mis en place chez Cyrus) [8].

Les cabinets ayant tiré parti de ces outils digitaux ont pu prendre des parts de marché pour se développer rapidement, ainsi qu’améliorer leur ROI (ROI compris entre « 25 et 40 % de croissance organique d’ici septembre 2020 » pour Equance) [8].

En revanche, si plus de la moitié (56%) des clients se disent intéressés à utiliser davantage d’outils numériques et virtuels à l’avenir (surtout les millennials et les membres de la génération X), la relation physique reste importante pour ce métier. Lorsqu’il s’agit de trouver réponse à des interrogations ou de planifier les plus grands moments de la vie, les clients manifestent un plus grand intérêt à préserver des interactions personnalisées et authentiques avec un vrai conseiller [6]. Le challenge sera de trouver le bon équilibre entre les outils numériques et les conseils en face à face.

Découlant de l’hybridation du métier :

Les robo-advisor

La digitalisation du métier a permis l’émergence des robo-advisor. Ce sont des plateformes digitales entièrement automatisées. Dans le cadre de la gestion de patrimoine, ils assistent à l’aide d’algorithmes et certains peuvent même conclure quelques opérations financières à la place du client. En plus, ils demeurent disponibles à toute heure et à n’importe quel jour [7].

S’inscrivant dans le cadre de l’hybridation du métier soulignée plus haut, ils ne remplacent pas totalement l’intervention humaine, mais ils assistent les conseillers à mieux se concentrer sur les objectifs principaux. La substitution, par rapport à l’enregistrement des données par exemple, aide drastiquement dans cette optique [7].

La synchronisation des services

Avec le développement de solutions digitales de gestion de patrimoine, la clientèle peut, à présent, directement gérer son portefeuille patrimonial.

Dans le cadre d’un modèle hybride de gestion de patrimoine, le challenge sera de correctement synchroniser les diverses entrées disponibles à travers la multiplicité d’appareils digitaux, et le partage digital/physique d’informations. Cela implique la nécessité d’une meilleure connectivité entre le conseiller et la clientèle à travers ces divers points d’entrées [7].

3 – BUSINESS

Importance accrue du conseil pluridisciplinaire

Les CGP veulent placer les missions de conseil au cœur de leur activité, dans un rôle comparable à celui d’un médecin de famille. En se plaçant en opposition aux conseillers bancaires, une relation impersonnelle et changeant régulièrement, les CGP souhaite promouvoir une relation de confiance durable avec leurs clients [3].

C’est ainsi que les CGP interrogés dans le cadre de l’étude Apredia « considèrent que leur rôle va se renforcer pour aider leurs clients à définir leurs objectifs patrimoniaux ». Ce sont donc des missions de conseil « qu’une majorité de CGP souhaite mettre particulièrement en valeur dans les mois à venir en essayant de développer plus qu’aujourd’hui une rémunération en honoraires de conseil » [5].

La nature de leur conseil évolue également, et leur champ de compétences dépasse désormais la traditionnelle sphère financière. De mieux en mieux formés, anciens fiscalistes, notaires, avocats ou banquiers privés, ces professionnels sont désormais nombreux à maîtriser les différentes disciplines qui composent le métier : droit, fiscalité, finance et immobilier [3].

Concentration du marché

Signe de maturité de l’industrie, on observe une concentration du marché de la gestion de patrimoine, surtout au niveau des grands acteurs régionaux (ex. Astoria Finance qui rachète Les Comptoirs du Patrimoine) [3].

Celle-ci est liée à l’augmentation des coûts liés à la réglementation ainsi qu’à l’acquisition d’outils digitaux et de systèmes d’information plus performants [3].

Grâce au partage des savoir-faire technologiques [1] et la mise en commun des connaissances par spécialité ou par outil [2], cette concentration répond à plusieurs nécessités :

Amortir le choc Covid [1]

Améliorer l’expérience client [1]

Pérenniser et améliorer la résilience durable de l’activité [2]

Segmentation du marché

La concentration du marché met en lumière une segmentation de ce dernier entre d’un côté des cabinets de gestion de patrimoine qui cultivent une vision entrepreneuriale et dont le principal objectif est de continuer à grandir, et de l’autre, des acteurs qui entretiennent un esprit « profession libérale », des cabinets de taille plus modeste qui se sont constitué une base de clientèle très fidèle [3].

En termes de taille, selon les données publiées en 2018 par l’AMF, la grande majorité des encours gérés est captée par les quelque 50 cabinets les plus importants qui, à l’instar de Crystal, Olifan Group, Cyrus Conseil ou Astoria Finance, réalisent la moitié du chiffre d'affaires [8]. Les 4 641 cabinets de conseillers en investissements et CGP indépendants en France, quant à eux, gèrent environ 12 % de la collecte et 10 % des parts de marché pour un chiffre d’affaires total de 2,6 Md€ [8].

Diversité des modèles de croissance

Si la croissance externe est particulièrement importante dans ce marché, comme souligné précédemment, elle est loin d’être le seul modèle de développement pour les cabinets. Parmi les cabinets les plus importants, certains se sont développés grâce à une croissance organique très forte liée à leurs qualités techniques, commerciales et managériales [8].

Par exemple, Witam MFO a misé sur un modèle d’incubation : leur croissance organique s’est faite en association avec de jeunes gérants qui ont créé leur cabinet. Ils s’associent avec eux en mettant à leur disposition leur compétence en matière d’ingénierie. En échange, Witam prend une participation de l’ordre de 30 % dans leur capital car le but est de développer leur chiffre d’affaires pour qu’ils puissent conquérir leur propre clientèle.

Renouvellement générationnel

La profession de CGP est à un carrefour : d’un côté se trouvent les professionnels matures, qui tiennent les rênes du métier, avec une forte expérience. De l’autre, la nouvelle génération, tout juste diplômée, avec une formation aboutie, mais une expérience moins développée [2]. Face à une règlementation changeante (MIF II, DDA, PRIPS) qui engendre une nécessité de formation accrue, les jeunes conseillers bien formés compléteront bien l’expérience des professionnels matures dans les cabinets.

APPENDIX - SOURCES

1. « Vers un avenir plus digital et responsable pour les CGP ? », L’Assurance en Mouvement, Nov 2020.

2. « Les évolutions à venir pour le métier de CGP », Profession CGP, Août 2020.

3. « Conseillers en gestion de patrimoine : l’avenir leur appartient-il ? », Magazine Décideurs, Fev 2020.

4. « Gestion de patrimoine : la société française évolue, les épargnants également », Argus de l’assurance, Oct 2019.

5. « Assurance vie : quelles tendances pour la gestion de patrimoine ? », Argus de l’assurance, Oct 2020.

6. « Les quatre tendances clés en gestion de patrimoine », Conseiller, Juin 2021. Les chiffres proviennent d’une étude réalisée par EY sur 500 investisseurs canadiens.

7. « Fintech : Les tendances au sein de la gestion de patrimoine », Euodia, Juillet 2019.

8. « Les secrets de croissance des CGP stars », Gestion de Fortune, Avril 2019.